Reading your contract before you sign up for a merchant agreement is your last line of defense against being stuck in a bad deal. Here are our best tips for reading and understanding your merchant contract.

Frank has been writing about payment processing and business services since 2015. He is a retired Air Force officer and a former practicing attorney. He has a Bachelor of Science degree in Psychology from The Pennsylvania State University and a Juris Doctorate degree from the Ventura College of Law, and currently resides in Paso Robles, California.

WRITTEN & RESEARCHED BY Frank Kehl Frank has been writing about payment processing and business services since 2015. He is a retired Air Force officer and a former practicing attorney. He has a Bachelor of Science degree in Psychology from The Pennsylvania State University and a Juris Doctorate degree from the Ventura College of Law, and currently resides in Paso Robles, California. Expert Contributor

Shannon has been writing for Merchant Maverick about small business software and financing since 2015. She started writing professionally about business topics in 2005. Shannon has been featured in the Washington Post, Reader's Digest, US News, MSN, Yahoo Finance, Business Insider, and other publications. She has a bachelor's degree in English from San Diego State University and currently resides in San Diego, California.

REVIEWED BY Shannon Vissers Shannon has been writing for Merchant Maverick about small business software and financing since 2015. She started writing professionally about business topics in 2005. Shannon has been featured in the Washington Post, Reader's Digest, US News, MSN, Yahoo Finance, Business Insider, and other publications. She has a bachelor's degree in English from San Diego State University and currently resides in San Diego, California. Lead Staff Writer

Our content reflects the editorial opinions of our experts. While our site makes money through referral partnerships, we only partner with companies that meet our standards for quality, as outlined in our independent rating and scoring system.

Reading your proposed merchant services contract before signing up with a provider is crucial to ensuring that the contract’s terms align with what was promised by your sales agent. Failing to understand your contract can lead to costly mistakes and other issues that could have been prevented by taking the time to read the “fine print” in advance.

There are three significant benefits to reading your contract:

This article explains what merchant agreements are, their structure, and how to interpret essential clauses. It also provides examples of common contract language related to contract length, cancellation procedures, and penalties. Additionally, it identifies red flags for dishonest sales agents and offers strategies to deal with such situations.

Table of Contents

A merchant agreement is a document (or documents) that establishes a contract between a merchant and a merchant services provider. Contracts are agreements between two parties that establish the expectations and rules of behavior governing the relationship between them.

Every merchant services provider will have a contract that governs your relationship with them, including Square and other popular payment service providers (PSPs). If you see a provider claiming that it has “no contracts” on its website, what this really means is that you won’t have a long-term contract that commits you to keeping your account open for years at a time.

Your contract might also include separate agreements with third-party service providers, such as payment gateway providers, which need to be reviewed carefully .

Unlike many other vendors you deal with in your everyday life, most merchant service providers will allow you some leeway to negotiate the exact terms of your contract. In fact, many providers assume that you will try to negotiate a better deal and set their prices higher than what they’re really willing to accept. In this case, failing to negotiate for lower rates and more favorable terms can be an expensive mistake.

Here’s what Jeff Marcous, the Chief Evolutionary Officer of Dharma Merchant Services, had to say about merchant services agreements:

The merchant agreement issue is definitely complex and is pretty much dictated by the acquiring banks of the MSP/ISO. For our part, we have to go along with the boilerplate terms set down by either Wells Fargo or Synovus Bank, but we do have authority to delete certain clauses – like termination fees, etc. It’s kind of like clicking on the terms of agreement for an iPhone update – if you or I actually read (and understood it), we would probably gasp at what is being agreed upon, but of course, you could not continue to use their services even if you pushed back on something.

That said, probably the most important thing is for an agreement to explicitly offer the ability for the merchant to cancel at any time without penalty. Even then, the processor has the right to keep an account “open” for a period of time in order to process any chargebacks or malicious activity on the account.

At the same time, understand that your ability to change the terms of your contract is limited.

However, many of the most critical aspects of your contract are, in fact, negotiable. These include the following items:

Clauses imposing early termination fees (ETFs) or liquidated damages are the most common terms in a merchant services contract to be waived through negotiation. No one wants to be hit with a penalty for closing their account, and providers are often eager enough to get your business that they’ll waive the ETF as an inducement for you to sign up with them. However, you should never rely on a verbal waiver promised to you by your sales agent. Always get a written waiver, and keep a copy of it for your records. We’ve heard far too many complaints from merchants who were promised a waiver but then had the ETF automatically taken out of their bank accounts later on because the sales agent never passed the waiver information along to anyone else at the company.

Although they’re becoming less common, merchant account agreements frequently require an initial commitment of three years. However, you can often have this term waived if you ask for a month-to-month arrangement instead. Be aware that having a waiver to the early termination fee does not mean that your three-year term is also automatically waived. These two terms are often contained in separate clauses of your contract, and you’ll want written waivers to both of them to protect against being automatically charged recurring fees after you’ve closed your account early.

Although we consider tiered pricing to be the worst possible processing rate plan for merchants, it’s still the most commonly used type of pricing in the industry. Why? Because most merchants don’t know the difference between tiered pricing and interchange-plus pricing, which is both more transparent and more affordable. Many merchant services providers will try to set you up with tiered pricing, even though they also offer interchange-plus plans. Don’t fall for it! Always ask for an interchange-plus pricing quote, and be prepared to find a different provider if it isn’t offered to you. Note that if your provider of choice offers flat-rate or membership pricing or uses a standardized interchange-plus rate based on your monthly processing volume, you might not be able to negotiate a custom pricing quote unless your processing volume is extremely high.

Merchant account providers charge a host of recurring and incidental fees, all of which should be disclosed somewhere in your contract. While some of these fees can be reduced or eliminated through negotiation, many others cannot. For example, you can almost always count on having to pay chargeback fees, monthly account fees (although you can sometimes lower the amount), and any fees that your provider has to pass on to issuing banks or credit card associations (e.g., Visa FANF fees). Fees that can be waived or reduced include application fees, account setup fees, statement fees, and your monthly minimum.

Your ability to change the terms of your merchant services agreement will depend primarily on both the size of your business and your negotiating skills. Providers make more money and are exposed to less risk by working with larger businesses with established processing histories, so they’re more likely to adjust their offer to get one to sign up. Small or newly established businesses, on the other hand, don’t have these advantages and often have to take what they can get. However, you can still improve your negotiating skills and use them to your advantage, regardless of the size of your business. Check out our article on negotiating your credit card processing deal for some helpful tips.

Although most of the content in a merchant agreement will be very similar from one provider to the next, this won’t make the job of deciphering your contract any easier. No two merchant agreements are identical. Every provider has its own way of organizing its contracts. Some providers even have multiple versions of their contracts, depending on which backend processor is underwriting your account.

Merchant agreements can run anywhere from as few as four pages to over 60 pages, depending on how they’re organized and how many additional agreements are included with them. At a minimum, you can expect your agreement to include two distinct parts: a Merchant Application and a set of Terms and Conditions. You might also have one or more Third-Party Agreements as well, either incorporated into the main document or published separately. Here’s a breakdown of what to look for in each part of your agreement:

Before you can open a credit card processing account, you’ll need to fill out a Merchant Application. This document, often only one or two pages long, collects information about you and your business. You might also need to provide enough financial information for the provider to run a check on your personal credit.

One word of caution is in order here: providers often ask for information about your business bank account, including account and routing numbers. While they legitimately need this information to deposit funds from your credit card sales into your account, they can also take money out as well. Unscrupulous providers can sign you up for a merchant account without your knowledge and begin extracting any number of fees immediately, even if you don’t process any credit card sales. We recommend that you wait to provide this information until you’ve read your contract thoroughly and are certain that you want to open an account with your chosen provider.

Merchant applications also provide a space to lay out all the information that will be unique to your account in one location. This will include all applicable processing rates and recurring fees that vary from one merchant to the next. Incidental fees, which are typically the same for everyone, will usually be found somewhere in the Terms and Conditions portion of your contract. Here’s a sample Merchant Application from CardConnect to give you an idea of what to expect.

Merchant applications aren’t as chock full of legalese as the Terms and Conditions section of your contract, but it’s still critical to review them very carefully. One particularly important thing to look for is the presence of mid-qualified and non-qualified processing rates. This is a sure sign that your sales agent has signed you up for an expensive tiered pricing rate plan. Sales agents can mislead you by only verbally disclosing the qualified rate for your plan, without mentioning the much higher mid-qualified or non-qualified rates.

Unlike your Merchant Application, the Terms and Conditions section of your contract includes all the stuff that applies equally to every merchant account maintained by the provider. And it’s a lot of stuff. Terms and Conditions sections invariably run for many pages and include a tremendous number of rules and policies that govern how you use your account, all spelled out in exacting legalese that can be painfully difficult to read.

Some providers have started to call this section a Program Guide, perhaps in an effort to make it sound a little less daunting. Most of the information contained here is industry-standard, with little variation from one provider to another. However, there are also some really important policies buried in here that can have a serious impact on your relationship with your provider.

In reviewing the Terms and Conditions of your merchant agreement, the following subjects are particularly important and should be read very carefully:

How long is your contract? Your sales agent should answer this question for you in detail before you sign up, but they don’t always do so. The typical, industry-standard merchant agreement has an initial term of three years, or 36 months to align with your account’s monthly billing cycle. While a three-year initial term is the most common, we’ve seen contracts where this term is as short as one year and occasionally as long as four (or even five) years. Automatic renewal clauses extend the term of your contract, typically for an additional twelve months at a time. Again, there’s some variation among providers, with subsequent terms ranging from six months to two years at a time. Note that Canadian law limits contract extensions to no more than six months at a time.

Long-term contracts have always been unpopular with merchants, as they make it very difficult to get out of your contract if you want to switch providers. The trend within the industry now favors month-to-month billing, which is much more flexible. Be aware, however, that you are still under a commitment even with month-to-month contracts. Look for verbiage in your Terms and Conditions that specifies an initial term of 30 days, with automatic renewal periods of an additional 30 days at a time thereafter. With no early termination fee imposed, month-to-month contracts allow you the freedom to close your account at practically any time without penalty. At most, you might have to pay recurring fees for one additional billing cycle.

One of the worst aspects of merchant agreements is when providers impose an expensive penalty for closing your account before the end of the current term. The most common practice is to charge a fixed early termination fee (usually between $295 and $495), regardless of how much time is remaining on your current contract term. Some providers will offer proration based on the number of years left on your contract, which lowers (but doesn’t eliminate) the penalty if you stay with them for over a year or two. Providers may also use liquidated damages, which are based on a combination of your average monthly processing volume and the length of time remaining on your contract.

When you read the early termination provisions of your contract, one aspect that will probably upset you the most is the dramatically unequal way in which early termination applies between you and your provider. While you, the merchant, are contractually obligated to keep your account open for years at a time and pay a host of recurring fees, whether you use the account or not, your provider can close your account unilaterally at any time for practically any reason. While they’re highly unlikely to do so as long as they’re making money off of your business, a sudden closure could leave you unable to accept credit or debit cards until you can line up a new provider.

While lengthy contract terms and automatic renewal clauses are designed to keep you on the hook indefinitely, it is possible to close your account without penalty. Every merchant agreement contains specific instructions for closing your account. Providers don’t make it easy, but if you follow the directions in your contract very carefully, you can terminate your contract at the end of the current term without being charged an early termination fee or liquidated damages. Almost all providers require written notice of your intent not to renew your contract, provided within a specified number of days before the end of your current term. Unfortunately, providers often make it difficult to find out the exact date of your contract renewal, so you’ll want to pin this down and send in your notice well in advance of the minimum required period. Providers typically require 30 days’ notice, although we’ve seen some contracts where the required notice period was as long as 90 days prior to termination. You should also beware of providers that require that the notice be submitted on a special written form, which they jealously guard and will only provide to you upon request.

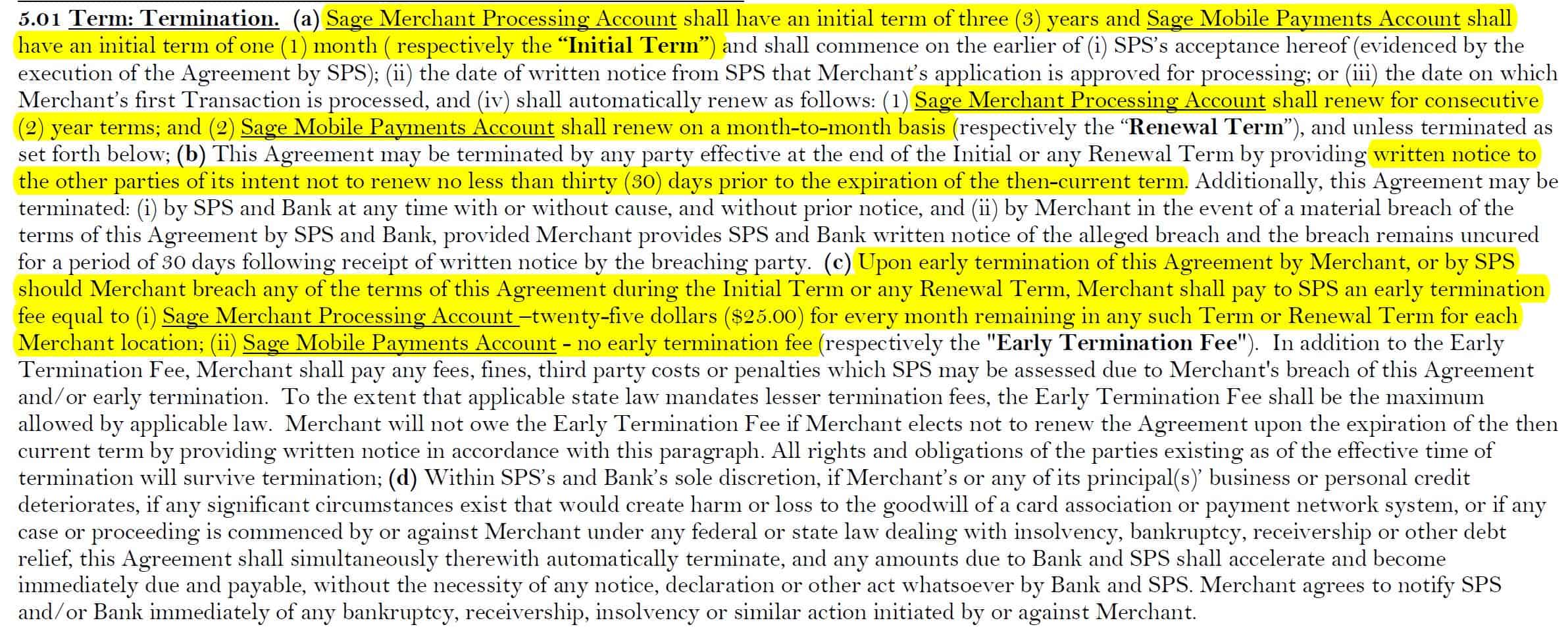

Here’s an extract from an old Sage Payment Solutions (now Paya) contract that includes examples of all the clauses and terms we’ve discussed above:

Legal disputes between merchants and their providers are always a possibility, and providers will attempt to protect themselves by including language in their contracts, which makes it more difficult for you to pursue this kind of remedy. Usually located near the very end of your Terms and Conditions, you’ll almost always find a few provisions that cover any type of legal action you might wish to pursue.

Mandatory arbitration clauses are the most common kind of limitation you’ll find, and they’re a standard feature of almost all merchant services agreements today. These clauses simply require you to submit to mandatory arbitration in lieu of filing a lawsuit. In most cases, courts will send you to arbitration prior to hearing your case anyway, so these clauses don’t have much impact on your ability to pursue a legal remedy.

Choice of jurisdiction clauses will usually limit jurisdiction to courts in the state where the provider is headquartered. While this doesn’t prevent you from pursuing legal action against them, it can throw up a significant roadblock if you don’t live in the same state. You’ll be responsible for any costs you incur traveling to court appearances, depositions, etc. While we don’t recommend that you choose a provider based solely on geographic proximity to your place of business, you should be aware of the impact this kind of contractual limitation can have if you end up trying to sue your provider.

If your merchant account includes a product or service provided by a third party, you’ll have a separate agreement with that party included as part of your contract documents. Payment gateways and equipment leases are the most common examples of these additional agreements.

Third-party agreements may be separate documents, or they may be included within the body of your Terms and Conditions. For example, if you need a payment gateway and your provider uses Authorize.Net (see our review) exclusively, you’ll have an agreement that applies between you and Authorize.Net.

With equipment leases, many providers will use a separate company to provide the equipment and administer the lease. In most cases, this “company” is actually a wholly-owned subsidiary of the provider, often located at the same physical address. Be aware that the length of your equipment lease is separate from the initial term of your merchant account agreement. In fact, it’s often longer – keeping you on the hook for monthly lease payments even if you close your merchant account at the end of the initial term.

Nowhere is the credit card processing industry sleazier and more dishonest than in the sales practices it employs to sign merchants up for accounts. Many providers lower their costs by relying on independent sales agents, who often work on a commission-only basis, and need to sell accounts to put food on the table. While there certainly are honest, experienced people working as independent sales agents, you’re more likely to encounter an agent who’s willing to take some ethical shortcuts in order to close the deal and sign you up for an account. Here’s a rundown of the most important “red flags” that can help you to identify and steer clear of a dishonest agent:

Being stuck in a long-term contract might not seem so bad when your business is humming along, but things can go south very quickly for a number of reasons. Maybe your processor has raised your rates, or you’ve had a bad experience with customer service. Maybe you’ve found a better provider with lower rates and no long-term contracts. Maybe you just need to close your account because you’re retiring, shutting down your business, or selling it.

Whatever the reason, early termination fees, and automatic renewal clauses can make it difficult to exit your agreement without paying a substantial penalty. Unless it’s an emergency situation where you need to get out of your contract immediately, we recommend that you wait until the end of your current contract term and close your account by following the specific instructions contained in your contract. The aim here is to give your provider sufficient notice that you won’t be renewing your contract, so it doesn’t auto-renew, and you won’t be assessed an early termination fee. Providers are notorious for making this process as difficult as possible, but as long as you get the ball rolling ahead of time, you should be able to submit the proper documentation and provide the required notice to end your contract.

If you’re only a few months into a long-term contract and it’s obvious that things just aren’t working out, closing your account without penalty will be more difficult. Providers are usually more willing to work with you in situations where the business is closing or changing hands, but if you’re just trying to switch to a competitor, they’re not going to help you out. However, the processing industry is so competitive that some providers will offer to pay your early termination fee for you if you switch to them. Just be aware that if you do this, you’re almost certainly going to be trading one long-term contract for another. If you’re going to switch providers, we recommend that you switch to a company that will offer you true month-to-month billing with no long-term commitment at all.

If you’ve had a really bad experience with your provider and can’t get out of your contract, you should consider filing a complaint against them with the BBB. Despite all the shady practices commonly found in the processing industry, merchant services providers are just as sensitive about their public reputations as any other business. We’ve seen plenty of situations where an aggrieved merchant went public with a BBB complaint, and the provider quickly released them from their contract and refunded their early termination fee.

Despite all these issues, having a merchant account and being able to accept credit cards is definitely worth the effort for most merchants. With customers increasingly relying on credit and debit cards for nearly all of their purchases, the additional sales that come with having a merchant account will usually more than make up for the hassle and expense of setting one up. The real trick, of course, is to identify and sign up with the provider that can offer you the best combination of low fees, reasonable contract terms, and high-quality customer service.

In analyzing your merchant agreement, the following suggestions can help you to avoid missing anything important:

You should read your contract thoroughly regardless of which merchant services provider you’re about to sign up with. Even with the most reputable providers, you’ll want to have a clear understanding of the obligations you’re undertaking when you sign your contract. At the same time, it’s important to understand that most of the problems we’ve discussed above will not be an issue if you sign up with a top-notch provider. The best providers in the industry fully disclose their pricing and contract terms on their websites rather than burying this information in the fine print of a contract. They also employ in-house sales teams who aren’t under pressure to earn a commission.

Finally, all of the best credit card processors for small businesses offer true month-to-month billing with no long-term contracts or early termination fees.

Frank has been writing about payment processing and business services since 2015. He is a retired Air Force officer and a former practicing attorney. He has a Bachelor of Science degree in Psychology from The Pennsylvania State University and a Juris Doctorate degree from the Ventura College of Law, and currently resides in Paso Robles, California.